Regular listeners to the Dividend Talk podcast will often hear us talk about WBA. You might even listen to us call them a turnaround play.

What does that even mean?

The company even turned up on the famous Dogs of Dow in 2023. So is now the right time to buy Walgreens Boots Alliance (WBA)?

Before I get into that, you might recognize that my own blog over at EMF has gone a little stale. I haven’t been updating it in quiet a while. During Covid, It was much easier to maintain a blog and a podcast and write freelance for Sure Dividend. I don’t know about you, but after being locked up for some time, I appreciated doing the little things. I now try to spend as much time outdoors doing stuff with the family. All this means is that now my focus is purely on Dividend Talk and Writing for Sure Dividend. I will eventually do away with my Blog. But don’t fret; I will still write on this blog instead.

Okay, enough about me. Let’s move on to the task at hand and see what I will do with my WBA shares.

Quick Summary Of Walgreens Boots Alliance

I know not everybody has time to sit down and read a 20-minute blog post, so here is a quick summary of WBA for those in a rush.

Walgreens Boots Alliance (WBA) is a global pharmacy-led health and wellbeing company. The company operates in over 25 countries and has a diversified business model, focusing on retail pharmacy, pharmaceutical wholesaling, and healthcare services.

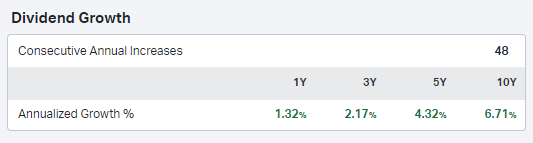

From a dividend growth perspective, WBA has a history of consistent dividend payments and increases. The company has paid dividends for over 100 years and has increased its dividend annually for the past 43 years, making it a Dividend Aristocrat.

The company’s dividend yield is currently around 5.2%, which is way above its historical average of 1.68%, which shows how far the price has fallen.

WBA’s dividend growth has been modest in recent years, with the company increasing its dividend by an average of 2-3% per year. This is lower than the industry average, but it is important to note that the company has invested heavily in its business to support long-term growth.

Overall, WBA is a well-established company with a strong track record of dividend payments and increases. While the dividend growth has been modest in recent years, the company is focused on long-term growth.

Two questions remain

- Can the company transform into healthcare?

- Can investors expect the company to continue paying dividends and increasing them over time?

Walgreens Boots Alliance Business Segments

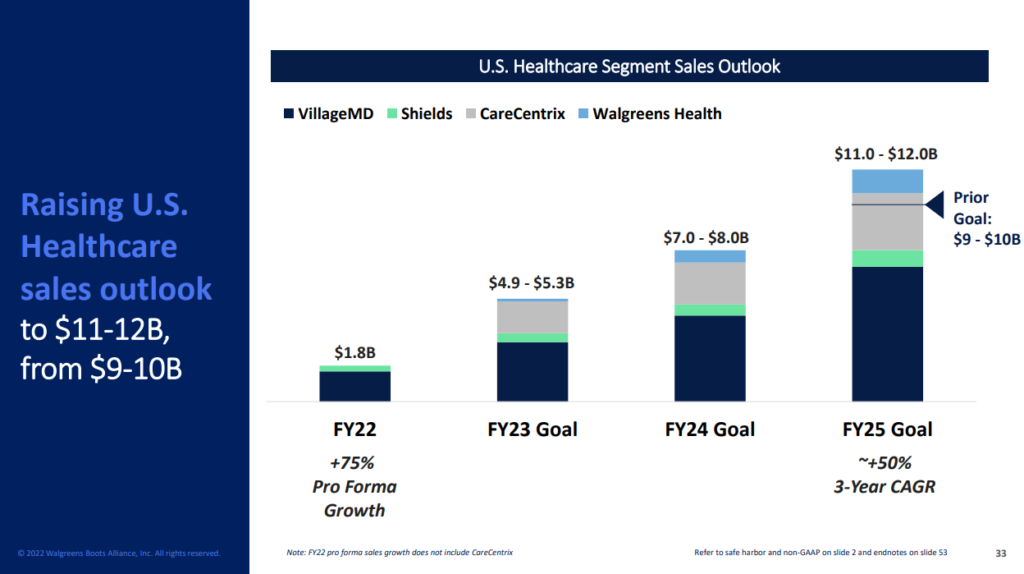

Walgreens Boots Alliance (WBA) operates in three primary business segments: Retail Pharmacy USA, International, and Healthcare. In the 2022 Annual Report, WBA stated that its segment sales were U.S. Retail Pharmacy $109.1 billion, International $21.8 billion, and U.S. Healthcare $1.8 billion.

The Retail Pharmacy USA segment

The largest segment with sales of $109.1 Billion in FY 2022. This segment serves retail drugstores in the United States, which includes the Walgreens and Duane Reade brands. This segment is the company’s most extensive. It offers customers various products and services, including prescription drugs, over-the-counter medications, health and wellness products, beauty products, and photo services. This segment also provides customers access to healthcare services, such as vaccinations, health screenings, and counseling.

The International segment

The second largest segment with $21.8 billion in sales in FY 2022. International operates retail drugstores in countries outside the United States, including the UK, Ireland, and other European countries. This segment operates under the Boots brand, a well-known and respected brand in the European market. The retail stores in this segment also offer a wide range of products and services similar to the Retail Pharmacy USA segment.

The US Healthcare segment

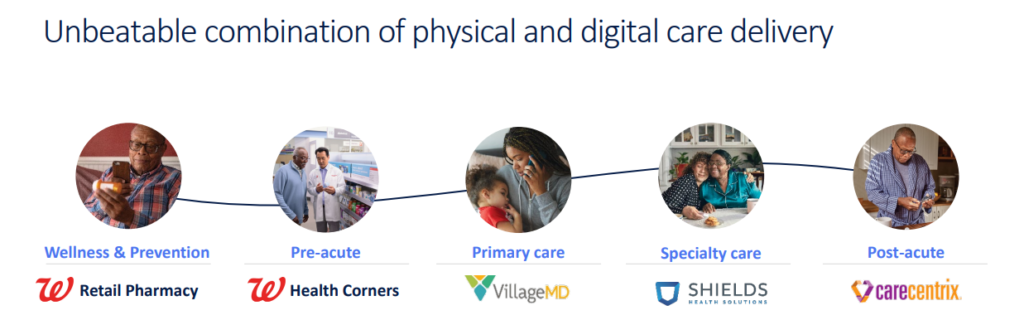

This segment was created at the beginning of 2022, which WBA calls a ” consumer-centric,technology-enabled healthcare business that engages consumers through a personalized, omnichannel experience across the care journey.”

In simple terms, US Healthcare is primarily VillageMD, Shields, and CareCentrix, which provide value-based primary care services for its customers.

Overall, WBA’s business segments are diverse and provide the company with a robust and balanced revenue stream. However, it is clear that they are a company in transition, reflected by the multiple changes in segments since I last wrote my article in 2020.

What does the company’s cash flow look like?

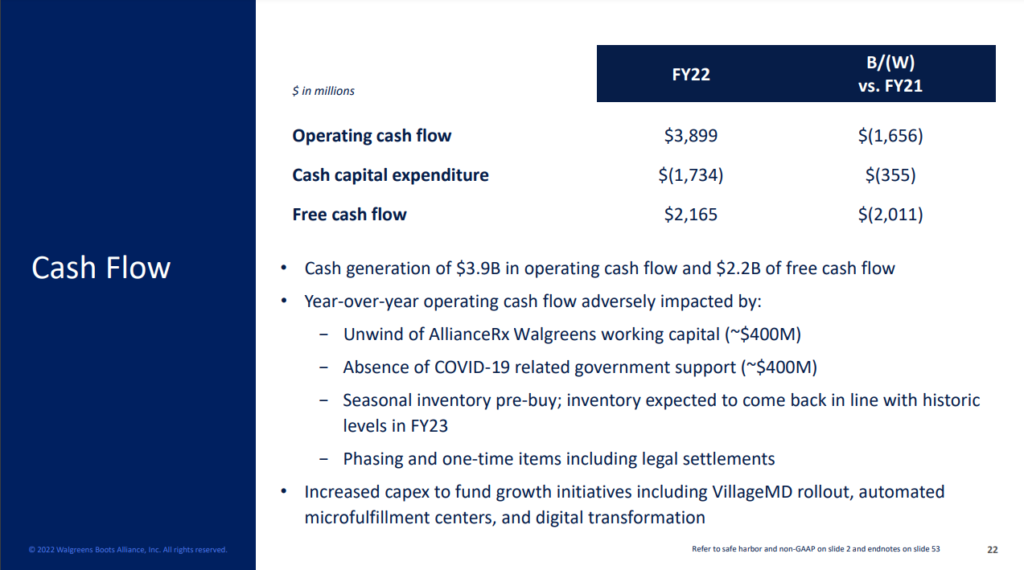

Free cash flow measures a company’s ability to generate cash after accounting for capital expenditures. I like to look at free cash flow as one of the leading indicators that a company can sustain its dividend. Strong Free Cash Flow with a low payout ratio is something dividend growth investors love to see.

Historically Speaking, WBA has generated positive free cash flow which helps fund its dividend. Since 2015, the company has generated between $4 and $6 billion, which allows it to fund its growth initiatives, pay dividends, and repurchase shares.

What happened the free cash flow in the last 12 months

However, that free cash flow took a nose dive in FT 2022, and the LTM figure looks even worse. So much so that the dividend is not even covered. While it doesn’t look pretty at first glance, we can attribute the sharp decline to opioid litigations that have plagued other companies such as CVS and Walmart. The company has agreed in principle to pay ~$6 Billion in Litigation charges and fees. While this is a lot of money and more than their typical free cash flow in a year, I don’t see this once-off expense changing the core business fundamentals and expect the company to recover to around $4 billion in FCF in the next 12 months.

The company’s payout ratio, which is the percentage of FCF paid out as dividends, is currently not covered. However, it is historically around 40%. This is a conservative payout ratio, which indicates that the company has a significant amount of room to continue increasing its dividends in the future. A lower payout ratio also suggests that the company has enough cash to invest in growth opportunities and weather economic downturns. I am more interested in the near future to see if they will hold the dividend or give a token increase to keep their dividend aristocrat status.

My guess is a token raise to $0.4815/Share a quarter in August.

What are Walgreen’s Growth Drivers

For Cash flow to grow, and WBA to continue grow its dividend, the company must have something that drives growth. Here are my thoughts on what could drive future growth:

Healthcare Services: WBA has been investing heavily in healthcare services, such as vaccinations, health screenings, and counseling. COVID-19 boosted these for a while, but demand is now normalizing. I would still expect health screenings to grow as people become more health-conscious. The Company plans to become a leading provider of local clinical care services by leveraging its consumer-centric technology and pharmacy network to deliver value-based care. The Company also intends to continue transforming its core pharmacy and retail business. The Company’s goal is to provide better consumer experiences, improve health outcomes and lower costs. To advance its healthcare strategy, the Company invested in VillageMD, Shields, and CareCentrix, which it believes will strengthen its capabilities in primary care, post-acute care, and home care.

Digital Initiatives: WBA has invested in digital initiatives like telemedicine and online prescription refills. These initiatives are expected to make it easier for customers to access healthcare services and products.

Smaller impact growth drivers

International Expansion: WBA operates in over 25 countries and has a strong presence in the European market. There is talk that they may offload boots when the right offer comes in. However, the company is expected to continue expanding internationally, particularly in emerging markets, which is expected to drive growth for the company’s International segment.

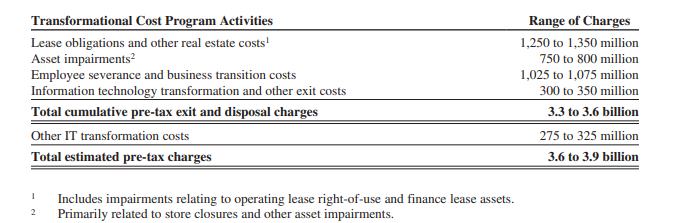

Cost Optimization: WBA has been focused on cost optimization to improve its financial performance, including closing some of its stores. The company has implemented measures to reduce costs in 2018 and is on track to save $3.5 Billion by FY 2024.

M&A: WBA has a history of making strategic acquisitions to expand its business and enter new markets like Village MD and Shields.

Competitive Advantages of Walgreens Boots Alliance (WBA)

Having a competitive advantage is important and can fuel future growth. But what sets Walgreens apart?

Strong Brand: WBA operates under the well-known and respected Walgreens and Boots brands, which gives the company a substantial competitive advantage in the retail pharmacy market. In Europe, particularly Ireland and the UK, Boots and their brands are well-known and widely used. Approximately 78% of the population of the U.S. lived within five miles of a Walgreens or Duane Reade retail pharmacy.

Diversified Business Model: WBA’s diversified business model focuses on retail pharmacy and healthcare services. This diversification allows the company to generate stable revenue and earnings and mitigate risk. Although at the moment, the healthcare segment does not generate enough revenue to make a meaningful impact.

Extensive Store Network: WBA operates over 12,000 retail stores worldwide and has a robust online presence, which allows the company to reach a large customer base.

Healthcare Expertise: WBA deeply understands the healthcare industry and has effectively navigated the rapidly changing healthcare landscape.

Why do we call Walgreens a Turnaround play?

Throughout the FY 2022 Annual report and Q4 Presentation, Walgreens makes no secret that they are transforming into a healthcare-driven company. The top line is stagnating a little bit, and their margins are under pressure and have been declining steadily over the last ten years.

To build its next growth engine, the Company has put its eggs in VillageMD, Shields, and CareCentrix, which it believes will strengthen its primary care, post-acute care, and home care capabilities. The company hopes that by FY 2025, the healthcare segment will drive sales of around $11 billion. This seems quite ambitious, but the company is confident it can meet this target.

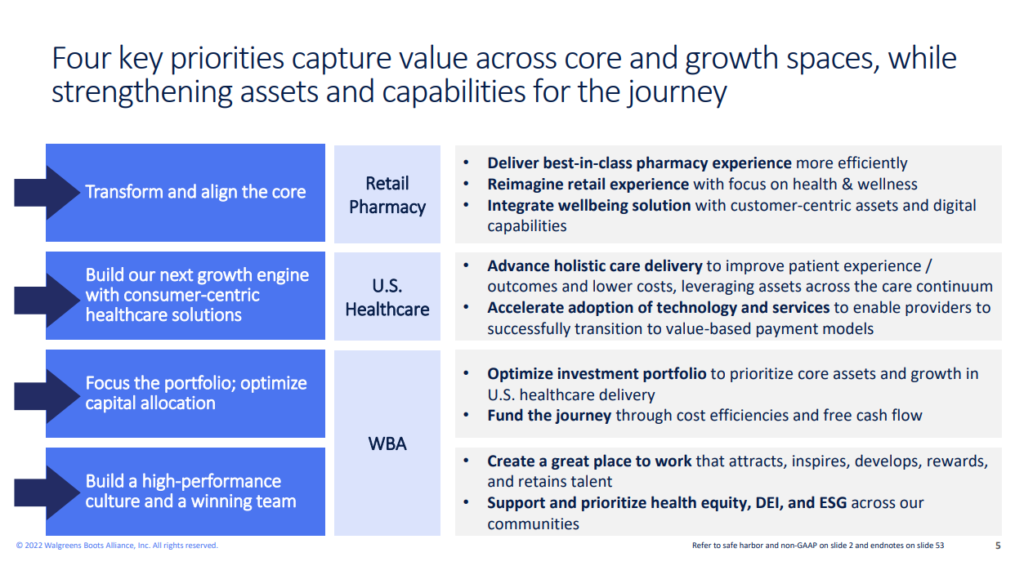

New CEO Roz Brewer, who was highly thought of while a COO of Starbucks, seems to have a clear vision and has identified her four key priorities. I like that the company has a clear direction and a leader who knows what she wants, but I am unsure how long it will take them to build this next growth engine.

What am I doing with my shares?

Please see my disclaimer before reading on. These are my thoughts and are not to be used as investment advice. I am simply outlining my thought process when deciding if I should buy a company or not. Please do your own due diligence and check all data for your self.

Currently, WBA is a top seven position in my dividend growth portfolio. I bought them for an average price of $46.8, which gives me a yield on cost of around 4.1%. It also means that excluding dividends, I am down ~ 22% or around 17% if I include the dividends I have received.

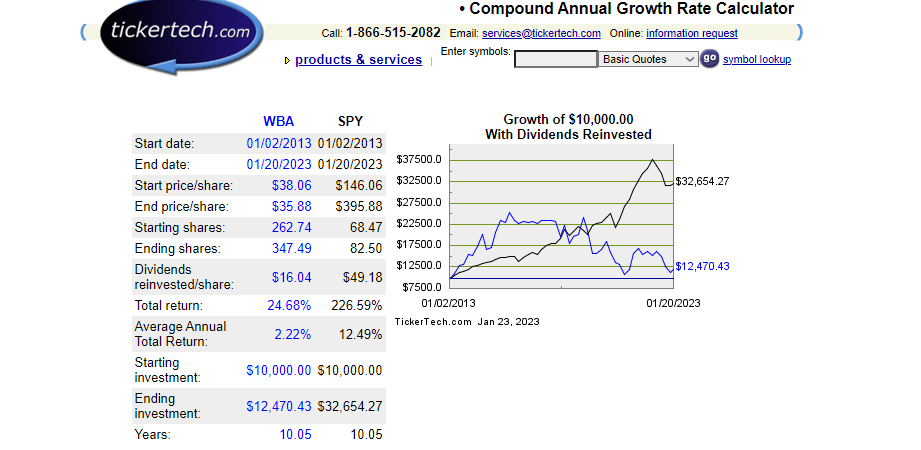

The share price doesn’t bother me as I am confident the company can generate steady revenue and return to around $4 billion in free cash flow. The problem with WBA is Dividend growth. It has declined steadily over the last ten years, and we will have another meager raise this year. Also, if you compare the total return of Walgreens against the SPY over the last ten years, it makes for some grim reading. 2.22% Average Annual total return with dividends reinvested versus 12.49% of SPY. The numbers are even worse since I bought them.

Final Thoughts

That said, I am unwilling to sell Walgreens at a loss at the moment. I believe WBA dividend is safe, and I also think that the company is trading below fair value. The company seems out of favor with the market over the last few years, and with the recent opioid settlement, cash flow has been affected in the short term. I’m not surprised the company is trading at multi-year lows.

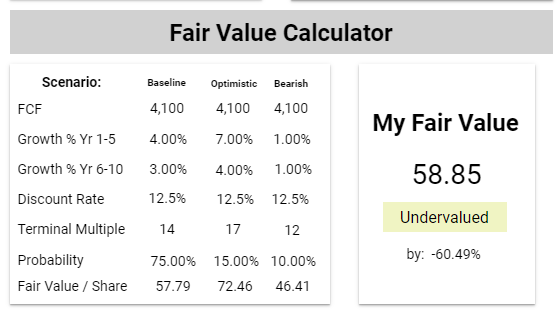

However the new CEO appears to have a clear vision and the healthcare segment has the potential to kickstart growth again, especially with an ageing population. Assuming FCF returns to its mean of ~$4 billion, I calculate the fair value price of the company in a range of $46 (Bearish) to $72 (Bullish) with a midpoint of $58. That leaves some room for multiple expansion and should give me an opportunity to reacess the company once they go above my average price per share.

While there is interest in the transformation of Walgreens and plenty potential, If I did not own any shares of Walgreens, I would not be in any hurry to buy them. I would wait to see how the healthcare segment grows compared to the companies projections. There will be ample time to buy the company over the next two years until cash flow stablisizes and begins to grow again. I would also like to start seeing them make some decent dividend raises.

Want to go deeper on dividend stocks?

100+ stock deep dives, dividend safety scores, and a stock card library built for European investors. Developed by Derek and Edgi.

You might also like

Reliable Dividends From A Foundational U.S. Portfolio

Why These Dividend Stocks Should Be in Your Portfolio You've come to the right place if...

Oct 23, 2024

Read article →DRIP Investing in Europe: Does Dividend Reinvestment Work Here?

You have heard it said that dividends are only half the story. The real power comes...

Apr 13, 2026

Read article →Retiring on High-Yield Dividend Stocks

Are you dreaming of retiring early? High-yield dividend stocks could be just what you need! By...

Nov 6, 2024

Read article →

Thank you for the analysis. As a European dividend investor how does tax loss harvesting factor into your decisions? Are you able to consider a WBA sale at a loss in order to perhaps offset some income taxes or a sale of another security that may have had an outsized price increase?

It is still a bit early in the year to look at tax loss harvesting. For me to do that, It would mean I would be after selling a different company at a profit. When I was doing options and buying and selling shares it was possibly more of a factor to reduce my tax liability and I have done this in the past but this year I’m shifting more focus to buying and holding which means tax loss harvesting won’t make sense. to my knowledge in Ireland, I cant offset it against dividend income, only capital gains so it makes no sense