Is Dividend Investing Irrelevant?

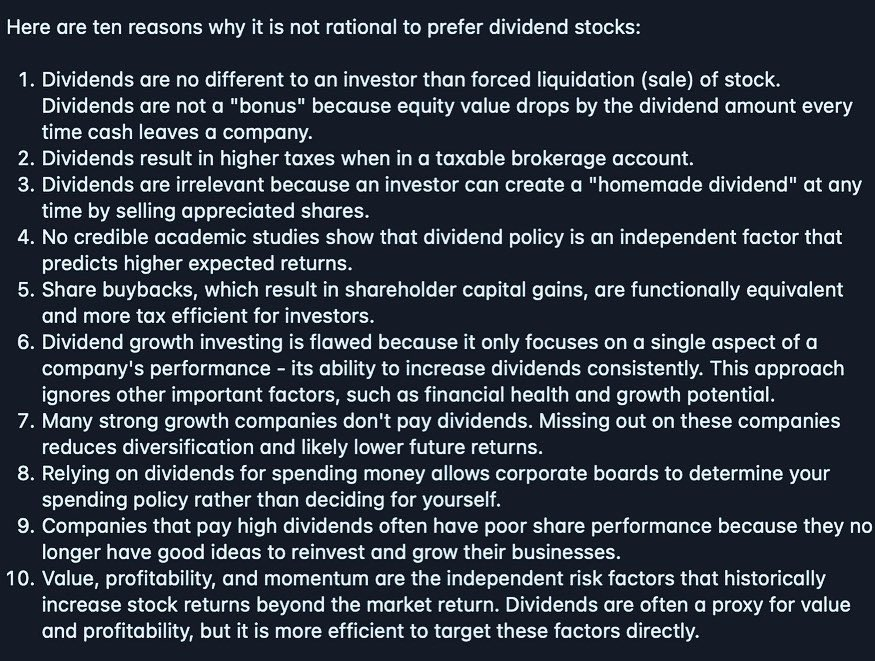

Let’s be honest I may be a little bit biased here. But recently, I received an Image with ten reasons why it is not rational to prefer dividend stocks.

This brings up an important question: Is Dividend Investing Irrelevant?

I received this image on Twitter, which inherently is not the best place in the world for a debate, so I thought it would be a fun exercise to think through each of the ten reasons and give my thoughts.

I plan on being as objective as possible, but I will be answering through my own experience, so I can’t promise to be 100% objective.

Just to reiterate right off the bat that, dividend growth investing might be right for you. Everybody’s Circumstances, Risk Tolerance, and Capabilities are different, and if you are unsure of anything, please seek professional financial advice.

Dividends are no different to an Investor than a forced liquidation of stock.

Dividends are no different to an investor than a forced liquidation of stock. Dividends are not a “Bonus” because equity value drops by the dividend amount everytime cash leave a company

So, Dividends and forced liquidation of stock are different in several ways:

- Dividends are payments made by a company to its shareholders as a portion of its profits. Forced liquidation occurs when a lender (Broker) sells a borrower’s (Investor) assets (Shares).

- Dividends are usually paid regularly (e.g., quarterly or annually), while forced liquidation is a one-time event.

- A forced liquidation may lead to a sharp decrease in stock price.

- Dividend payments are a voluntary action by the company, while forced liquidation is involuntary.

Ok, Ok, I know I answered this quite literally so far, but I think it’s important to understand the difference. I think it’s pretty clear that receiving dividends and a forced sale of your stock is completely different. However, I want to tackle the part where it states that dividends are not a Bonus.

In theory, this is correct, On the opening bell of the Ex-dividend date, you will notice that the company’s share price will almost certainly be lower. I say “Almost certainly” because there are sometimes exceptions, but in general, the price will drop before the market opens. The amount of the drop is not always the same as the dividend amount. Sometimes it’s more, and Sometimes it’s less.

However, no one knows where the price will end up at the closing bell. Never mind where the price will be in 10 years. There is no guarantee that if a dividend weren’t paid, the companies price would keep going up.

Remember, the share price is affected by many different things with no guarantees, I am happy to pick up my Bonus” in lieu of short-term equity value as no one knows where the long-term equity value will end up.

Dividends Result in Higher Taxes

Dividends result in higher taxes where in a taxable brokerage account

Taxes are a funny subject (and No Offence intended), but blanket statements like this usually come from across the Atlantic. However, In Europe, dividends are taxed differently depending on the country. I am from Ireland, so that I can speak from an Irish perspective, but I know for a fact we have different taxes than the Netherlands or Poland.

Here are a few common tax advantages of dividends in Europe (That I am aware of):

- Dividends may be taxed at a lower rate than other forms of income in some countries. In Ireland, the lower income tax on dividends is 20% while the capital gains tax is 33%. ( Although you do have a small allowance here)

- Some countries may offer tax credits for dividends received, reducing the overall tax liability. ( We don’t have this in Ireland)

- Europe has many double taxation agreements, which aim to prevent the same income from being taxed in two different countries.

- In some countries, dividends received by certain types of entities (e.g. pension funds) may be exempt from tax.

While the person posting the image might be right based on where he is domiciled, It is completely wrong (and maybe unintentionally arrogant) to believe everybody’s tax circumstances are the same.

It’s important to note that tax laws are subject to change, and specific tax implications may vary based on an individual’s circumstances. It’s recommended to consult a tax professional for advice on the tax implications of receiving dividends.

Dividends are irrelevant because an investor can create a “Homemade” dividend.

Dividends are irrelevant because an investor can create a “Homemade” dividend at any time by selling appreciated shares

The argument that dividend growth investing is irrelevant because an investor can create a “homemade” dividend by selling appreciated shares is flawed in my opinion for several reasons:

- While it is true that an investor can sell shares to create a “homemade” dividend, they must do so at a time that is convenient for them. This may not always align with their investment goals or cash flow needs. On the other hand, dividends are paid out on a set schedule, providing a more “reliable” source of income.

- The sale of appreciated shares may result in a capital gains tax liability ( as discussed above), which can reduce the overall return on the investment. Dividends, on the other hand, are often taxed at a lower rate than capital gains.

- By selling shares to create a “homemade” dividend, the investor may be missing out on potential future gains from the stock. This opportunity cost can reduce the overall return on the investment.

- Selling shares to create a “homemade” dividend may not always be a practical option, especially in a bear market when stock prices are declining. I would genuinely love to hear from people who are retired or close to it and had to sell shares during the last 18 months.

No credible academic studies

No credible academic studies show that dividend policy is an independant factor that predicts higher returns

Honestly, I did not study finance in university, so I care little about academic studies in this area. But It was not hard to find them. ( You can find anything to back your point of view if you look hard enough)

But Yes, there is academic literature that suggests that dividend policy is an independent factor that predicts higher returns. Several empirical studies have shown that stocks with a consistent history of paying dividends have outperformed stocks that do not pay dividends or pay irregular dividends. For example, a study by Michael O’Sullivan published in the Journal of Portfolio Management found that a portfolio of high-dividend-yielding stocks outperformed a portfolio of low-dividend-yielding stocks over the long term.

However, It is important to note that the relationship between dividend policy and stock returns is complex and can be influenced by several factors, including the overall market conditions, company-specific factors, and individual investor preferences. Personally, I believe that the relationship between dividends and stock returns is hard to quantify regardless of academic studies or not.

I did mention you can find any study to support your point of view. I just never said I would agree with them 🙂

My challenge would be for anyone to give me one single independent factor that predicts higher returns.

Share buybacks, which result in shareholder capital gains, are functionally equivalent.

Share buyback, which result in shareholder capital gains are functionally equivalent and more tax effecient for investors

I want to say that I understand where the author is coming from, and I also like when a company repurchases shares.

Share buybacks can play a role in increasing a company’s stock price, but it is not a guarantee and should be considered as one of many factors that influence a company’s market value.

The argument that share buybacks resulting in shareholder capital gains are functionally equivalent and more tax efficient for investors compared to dividends is flawed for several reasons:

- Share buybacks can be discretionary and may not occur consistently or regularly, whereas dividends are usually paid on a set schedule. This can make dividends a more reliable source of income for investors.

- Share buybacks increase the demand for a company’s stock, which can drive up the price, but they don’t provide investors with cash that they can use to meet their financial obligations. Dividends provide a cash return to investors, which can be more beneficial for those who need a regular source of income.

Share buybacks can signal to the market that the company’s management believes that its stock is undervalued, which can boost investor confidence. But the key here for me is valuation, I do not want to see a company that is grossly overvalued buying back shares.

Share buybacks don’t always increase the price.

Also there have been many companies that have repurchased shares but have seen their market value decrease. While share buybacks can boost earnings per share and increase demand for a company’s stock, they are not a guarantee of increased market value.

There are several reasons why a company’s market value may decrease despite share buybacks:

- If a company’s financial performance deteriorates, its market value may decline regardless of share buybacks.

- Changes in industry trends or technological advances can impact a company’s competitive position and financial performance, leading to a decrease in market value.

- Economic conditions and market sentiment can also impact a company’s market value, regardless of share buybacks.

- Companies may buy back shares to boost their earnings per share and meet Wall Street expectations, even if the buyback is not in the best interest of the company’s long-term growth.

Dividend Growth Investing is flawed because it only focuses on a single aspect.

Dividend Growth Investing is flawed because it only focuses on a single aspect of a company’s performance.

Of all the points the Author made, This is the one I disagreed with the most. First of all, listen to our podcast (Cheeky little plug ), and you will know this is not true. Dividends are probably the last item we focus on.

I prefer companies with healthy balance sheets, strong cash flow, robust business models, strong growth drivers, etc. Maybe the person who posted the ten reasons why Dividend Growth Investing is Irrelevant was speaking to the wrong type of investor.

With solid fundamentals, The dividends will come.

Many Strong companies don’t pay dividends.

Many Strong companies don’t pay dividends. Missing out on these reduces diversification and likely lower future returns.

Finally, I can agree on something. There are indeed lots of strong companies that don’t pay dividends that would be a shame to miss out on. But there is no rule set in stone to say that dividend growth investors can’t invest in some of these companies. While the allocation may be lower than their dividend portfolio, I know lots of dividend growth investors who have shares in companies like Meta and Alphabet. But I agree investors should not miss out on these types of companies.

The only part I can’t entirely agree with is the obsession with returns and beating the market returns. If I can cover my current income from my 9 -5 with dividend income, then I don’t care about how likely my returns are to be higher or lower than the market. I (try) to focus on what I perceive to be high-quality companies based on my competencies, and my goal is income, not beating the market.

I would encourage you to read my friend and podcast co-host’s annual report to see how he has been performing against the market over the last couple of years.

Relying on dividends for spending money allows corporate boards to determine your spending policy.

Relying on dividends for spending money allows corporate boards to determine your spending policy rather than deciding for yourself.

In theory, Yes, The board decides the amount of dividends to pay out and when to pay them, and this can impact an individual’s ability to budget and plan their spending.

Individuals can choose to invest in other forms of income-generating assets, such as rental properties, which offer more control and stability in terms of their spending policy.

Additionally, investors can also choose to diversify their investments, which can help mitigate the risk of relying solely on dividends for their spending needs.

I have said it once, and I’ll repeat it, Just because the majority of your portfolio is of a specific type ( Dividend Stocks, Growth Stocks, ETFs etc), it does not mean you can not diversify and hold other types of assets. There are many different ways to create a portfolio that suits your own needs.

Companies that pay high dividends often have poor share performance.

Companies that pay high dividends often have poor share performance because they have no good ideas to reinvest and grow their business.

A company’s dividend yield is the annual dividend payment divided by its stock price. There are several reasons why a company may have a high dividend yield:

- Lower stock price: If a company’s stock price falls while its dividend payment stays the same, its dividend yield will increase.

- Increased dividend payment: If a company increases its dividend payment, its yield will rise.

- Maturing industry: Companies in mature industries, such as utilities and consumer goods, may have a higher dividend yield as they generate consistent profits and may have less need to reinvest in growth opportunities..

It’s important to note that a high dividend yield may not always be a sign of a strong investment. A company’s dividend yield can be artificially inflated if its stock price has fallen dramatically, which may indicate underlying financial or operational issues. Additionally, a company’s ability to pay dividends may also be affected by changes in its financial performance, regulatory requirements, or other factors.

Value, profitability, and momentum.

Value, profitability and momentum are the independent risk factors that historically increase stock returns beyond the market return.

Its true, Value, profitability, and momentum are factors that have been shown to historically outperform the market in terms of stock returns. However, they are not independent risk factors and can interact with each other and with other factors that influence stock returns.

Value investing is the strategy of buying stocks that are undervalued compared to their intrinsic value. Value stocks tend to outperform over the long term because they are often undervalued and can provide a margin of safety for investors.

Profitability is a measure of a company’s ability to generate profits. Profitable companies tend to be financially stable and have a lower risk of default, which can lead to higher returns for investors.

Momentum investing is the strategy of buying stocks that have recently performed well and selling those that have underperformed. The idea is that stocks that have been performing well are likely to continue to do so, while those that have been underperforming are likely to continue to do so.

It is important to note that these factors are not always reliable and that their performance can be influenced by market conditions, economic trends, and other factors. Additionally, investing based solely on these factors can result in higher risk and higher volatility, as well as missing out on potential gains from other factors that influence stock returns.

Dividends can play a role in increasing a stock’s price, but it is not a guarantee that they will increase the stock price beyond the market return. The stock price is determined by supply and demand in the market, and a company’s decision to pay dividends can impact both of these factors.

As a Dividend Growth Investor, Valuation and profitability are also important to me.

Conclusion

In some cases, I can understand the point that the poster of the original image was trying to make. However, I feel Like Investors who bash dividend growth investing do not understand the concept if you earn a 4% yield with a 6% dividend growth rate, then it is no different than a 10% growth in share price.

Ultimately the dividend is what we seek without having to sell your stake in the company. However, For most of us, it is not the core aspect of the business that we look at. A business must have strong Revenue Growth, Earnings Growth, Cash flow Growth, Healthy Balance sheets, and Future Growth Drivers and be at an attractive price if a company has all of the above and then pays a consistent and growing dividend, I am happy.

Disclaimer – Dividend Talk is not a licensed or registered investment adviser or broker/dealer. We are not providing you with individual investment advice on this site. Please consult with a licensed investment professional before you invest your money. This site is for entertainment, informational, and educational use only.

Any opinion expressed on the site here and elsewhere on the internet is not a form of investment advice provided to you. We use information, data, and sources in the articles we believe to be correct at the time of writing them, but there is no guarantee of their accuracy, completeness, timeliness, or correctness. We are not liable for any losses suffered by any party because of information published on this site or elsewhere on the internet. Past performance is not a guarantee of future performance. By reading this site or subscribing to it, you agree that you are solely responsible for making investment decisions in connection with your funds.